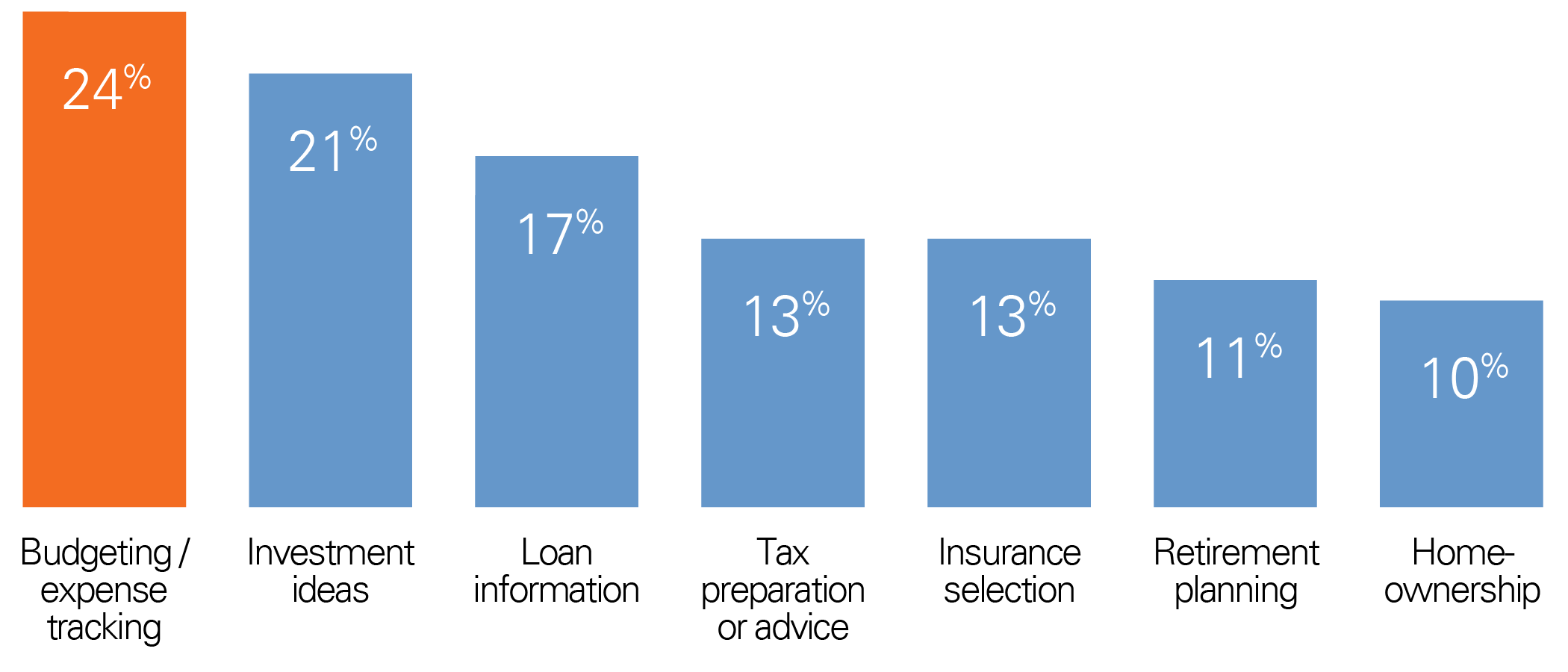

- Consumers are using conversational and generative AI to handle a variety of situations, including gaining insights into and managing their finances

- Debit cards are king, being used more than 1/3 of the days each month, but payments like mobile wallets and P2P are also leveling up with consumers

- Rates and rewards motivate consumers on which credit card to use, and when it comes to switching, 40% did so due to cash-back offers and 35% for better interest rates

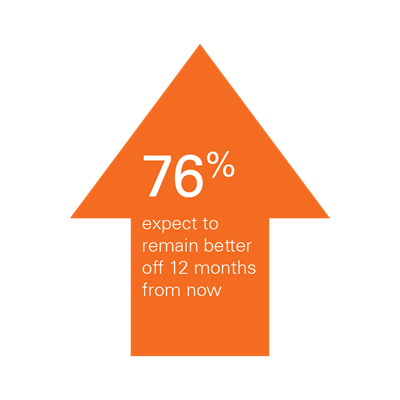

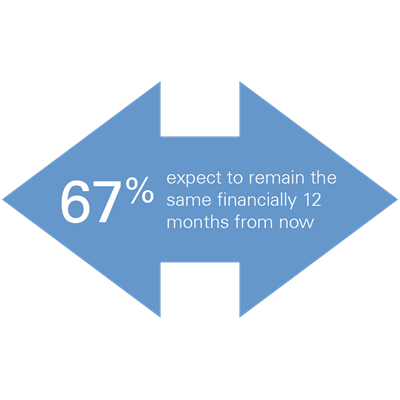

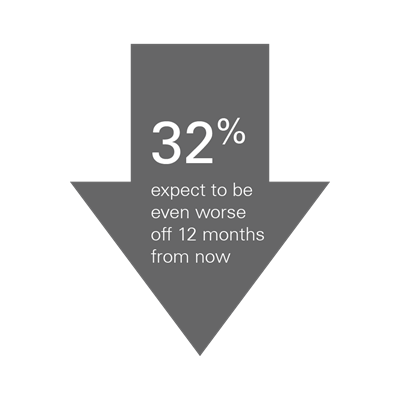

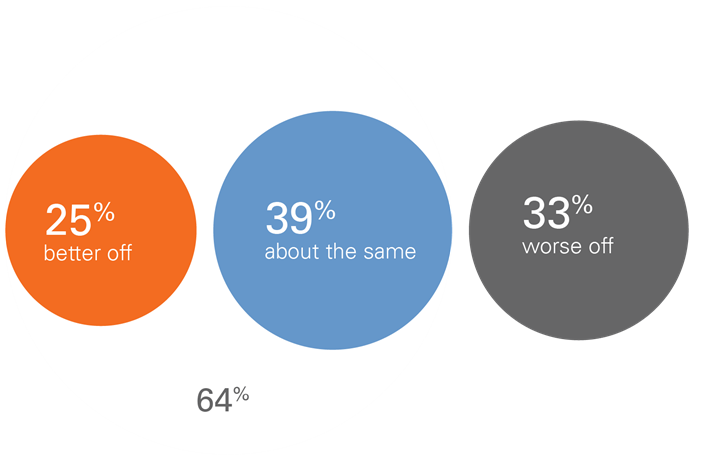

- Over 60% of consumers consider their financial situation to be the same or better compared to 12 months ago with income and expense changes as the top catalysts

Increase in AI adoption means increasing opportunities for financial service providers

Consumers’ generative AI financial uses

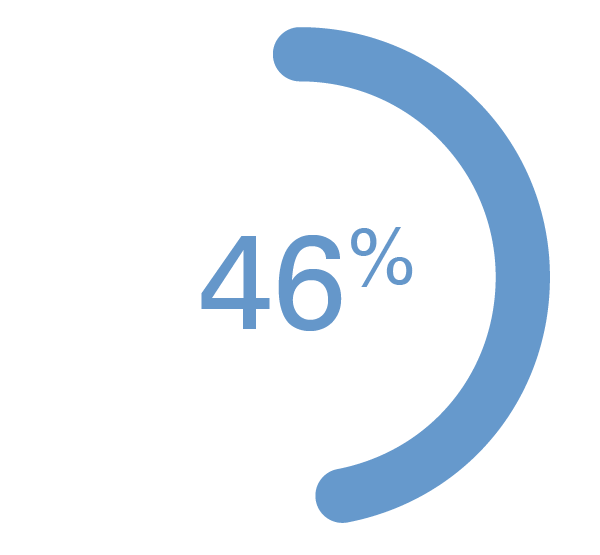

Even though interest and engagement with AI is strong, opportunity remains to improve comfort with financial institutions integrating AI into banking activities with 41% not comfortable with any AI-based banking tools.

Comfort with AI-based banking activities

Despite AI adoption, concerns remain

For many consumers, their biggest fears of AI mirror prior emerging technology trends over the past decade.

What do consumers have to say about AI helping them with their finances?

Consumers have their payment preferences for everyday purchases

Not all payment options are created equal. Debit, credit and cash are the methods consumers use most often while P2P and digital wallets have gained traction. And, while 37% of consumers have used checks and 13% have used BNPL in the past month, neither of those methods is among those consumers turn to most.

Most used payment methods

14% Cash

6% P2P

5% Mobile wallet

1% Check

Looking at the current state of credit cards

- How cards are being used

- Choosing the right card

- Why switch cards?

Why consumers use only one card versus multiple

Credit cards are commonplace

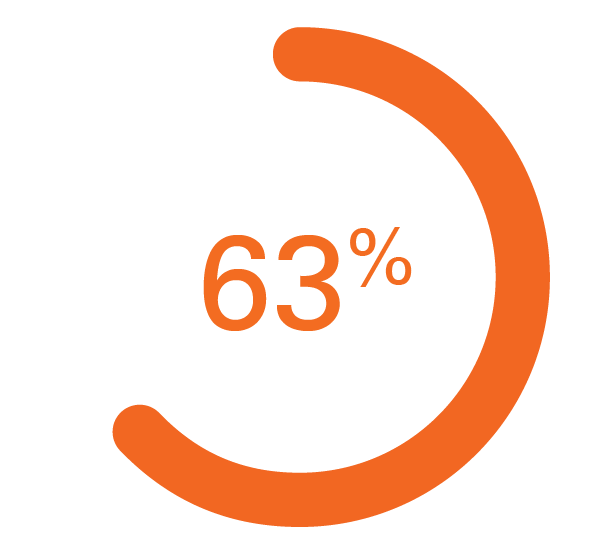

Credit cards influence consumers’ everyday purchases. Nearly two-thirds of consumers report having used a credit card in the past month and 62% of cardholders say they have used one in the last 7 days.

Whether carrying a single credit card or a wallet full of them, consumers are methodical when it comes to opening and using credit card accounts.

Why consumers choose to use a card for a particular purchase

Rewards drive card selection

Among multiple card carriers, rewards are the primary influencer when it comes to deciding what card to use for a purchase.

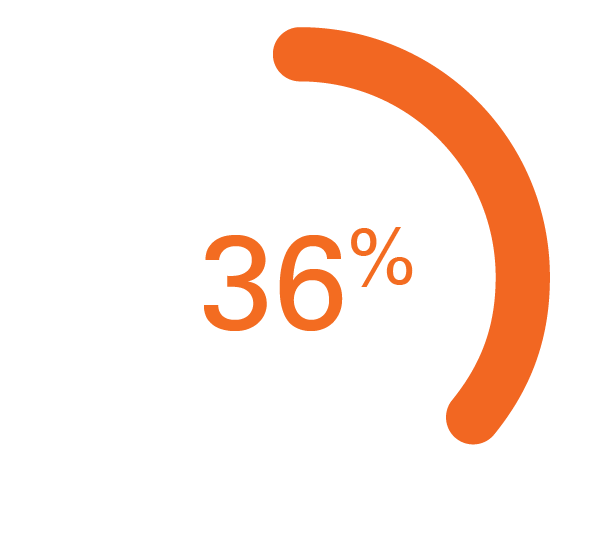

In fact, consumers are nearly twice as likely to look at the rewards they’ll receive from a purchase than the impact it will have on their current balance.

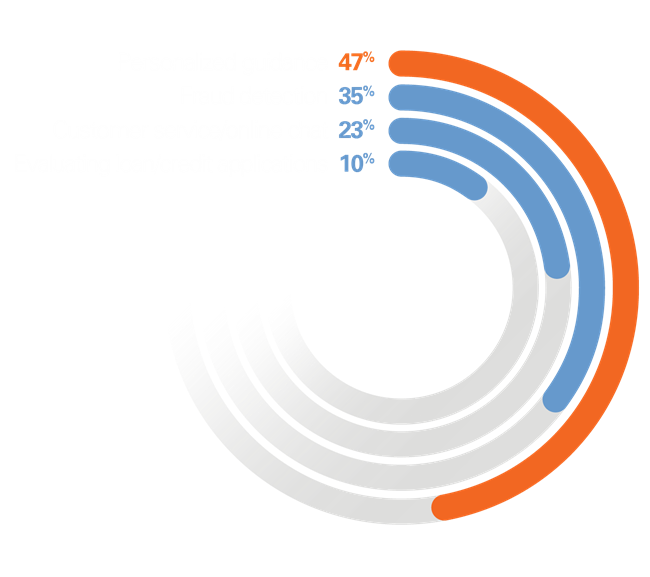

Why consumers switch cards

Card switchers look for value

Rewards aren’t just driving consumers to pick a certain card for a purchase, they are also one of the deciding factors when it comes to switching to a new primary card.

The top factor, however, is cash back. Four in ten consumers look at the potential for cash back when switching cards, followed by a better interest rate.

Consumers remain consistent with their financial outlook

What is driving these changes?